Insurance Needs at Different Life Stages

April 11, 2025 | Insurance

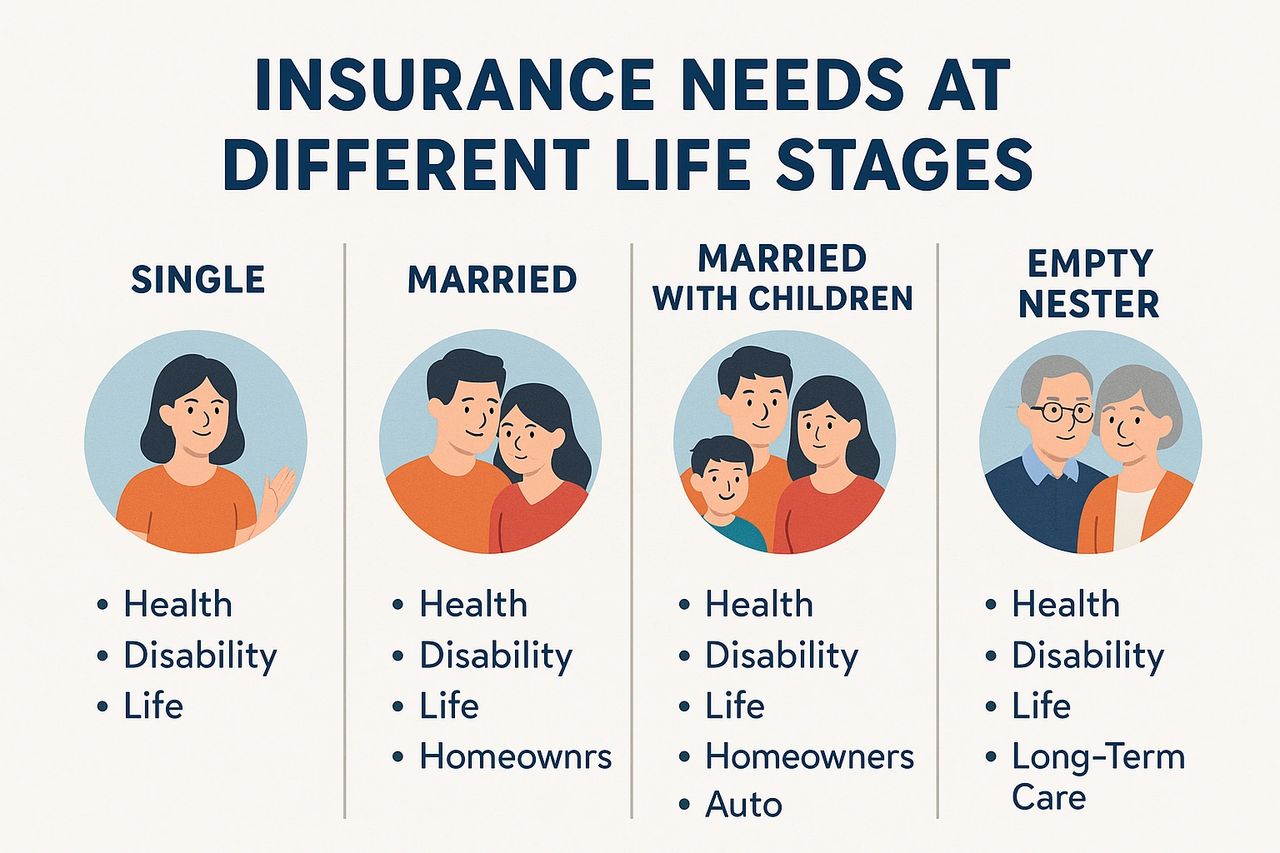

Life is full of changes, and as you progress through different stages, your insurance needs will evolve. Understanding the right types of insurance for each stage can help you stay protected and ensure you're not overpaying for unnecessary coverage. Whether you're living in Tempe, Phoenix, Scottsdale, Tucson, Gilbert, or Chandler, here's a look at the insurance coverage you might need as you navigate life's milestones.

In your 20s, you’re likely just beginning to establish yourself, which means your insurance needs will focus on protecting your health, belongings, and ability to earn an income.

Health Insurance: Health coverage is critical, especially in this stage when you might be leaving your parent's plan or starting your own. You’ll need to choose between individual plans or employer-sponsored options. Auto Insurance: If you own a car, auto insurance is a must. As a young driver, you may face higher premiums, but maintaining a clean driving record and taking advantage of discounts can help keep costs lower. Renter’s Insurance: If you're renting an apartment, renter’s insurance can protect your belongings from theft, fire, or water damage. It’s an affordable way to ensure your possessions are covered. Disability Insurance: This type of insurance helps protect your income if you become ill or injured and are unable to work. It’s a smart investment as your career begins to take off.

As you enter your 30s and 40s, your responsibilities often grow. You may have a family, a home, or a business, and your insurance needs will reflect that.

Life Insurance: If you have dependents, life insurance becomes a critical consideration. It ensures that your loved ones are financially secure if something happens to you. Term life insurance is often a cost-effective option for young families. Homeowners Insurance: As a homeowner, you need insurance to protect your property from damage and theft. This also includes liability coverage in case someone is injured on your property. Health Insurance: Your health insurance needs may become more complex as you age. You may require more extensive coverage, including options for family care or specific health needs. Disability Insurance: If you have a family or dependents, disability insurance is even more important in midlife. It helps protect your income if you're unable to work due to illness or injury. Long-Term Care Insurance: While it may seem early, some people in their 40s and 50s start thinking about long-term care insurance to cover future medical expenses, especially if they have a family history of chronic illness or other health concerns.

By the time you’re an empty nester, your insurance needs will shift, with more focus on your health and planning for retirement.

Health Insurance: As you approach retirement age, health insurance becomes a bigger concern, especially if you're planning to transition out of employer-sponsored coverage. Consider looking into supplemental health insurance or long-term care options. Life Insurance: If your children are financially independent, you may not need as much life insurance. You might want to adjust your policy to reflect any debts or estate planning needs instead. Long-Term Care Insurance: At this stage, long-term care insurance becomes a priority. This will cover the cost of nursing home or in-home care should you require assistance in the future. Homeowners Insurance: If your children are no longer living at home, you may decide to downsize or move into a new home. Make sure your homeowners insurance covers your new living situation and any changes in property value.

As you enter retirement, your insurance needs will be centered around ensuring your finances are secure and you’re prepared for any health-related issues.

Health Insurance: At this point, Medicare will likely become your primary health insurance coverage. However, you may still need supplemental insurance supplemental insurance to cover what Medicare doesn’t, such as dental, vision, or prescription drugs. Long-Term Care Insurance: If you haven’t already, consider purchasing long-term care insurance, which can help cover the cost of assisted living, nursing homes, or home care if needed as you age. Life Insurance: Life insurance can still be useful for estate planning and to leave a financial legacy to your family or charity. If you no longer have dependents, you may opt for a smaller policy or even consider canceling it. Homeowners Insurance: Your home may be paid off by now, but homeowners insurance is still important to protect your property and assets. Consider reviewing your coverage as you may no longer need as much coverage for things like personal liability. Medicare Advantage or Supplemental Plans: If you qualify for Medicare, you may also want to consider a Medicare Advantage Plan or Medigap policy to ensure you have comprehensive coverage as you age.

As you progress through life, your insurance needs will evolve based on your life stage, responsibilities, and future goals. Whether you're starting out in Tempe, Phoenix, Scottsdale, Tucson, Gilbert, or Chandler, understanding these shifts in your insurance requirements will help you make the right decisions for you and your family.

At Riseson Insurance, we’re here to guide you through each stage of life, helping you secure the right coverage at the best price. Call us at 602-460-5470 to ensure your protection for every phase of life.

1. Early Adulthood (Ages 18-30)

2. Midlife (Ages 30-50)

3. Empty Nesters (Ages 50-60)

4. Retirement (Ages 60+)

- Health Insurance: Health coverage is critical, especially in this stage when you might be leaving your parent's plan or starting your own. You’ll need to choose between individual plans or employer-sponsored options.

- Auto Insurance: If you own a car, auto insurance is a must. As a young driver, you may face higher premiums, but maintaining a clean driving record and taking advantage of discounts can help keep costs lower.

- Renter’s Insurance: If you're renting an apartment, renter’s insurance can protect your belongings from theft, fire, or water damage. It’s an affordable way to ensure your possessions are covered.

- Disability Insurance: This type of insurance helps protect your income if you become ill or injured and are unable to work. It’s a smart investment as your career begins to take off.

- Life Insurance: If you have dependents, life insurance becomes a critical consideration. It ensures that your loved ones are financially secure if something happens to you. Term life insurance is often a cost-effective option for young families.

- Homeowners Insurance: As a homeowner, you need insurance to protect your property from damage and theft. This also includes liability coverage in case someone is injured on your property.

- Health Insurance: Your health insurance needs may become more complex as you age. You may require more extensive coverage, including options for family care or specific health needs.

- Disability Insurance: If you have a family or dependents, disability insurance is even more important in midlife. It helps protect your income if you're unable to work due to illness or injury.

- Long-Term Care Insurance: While it may seem early, some people in their 40s and 50s start thinking about long-term care insurance to cover future medical expenses, especially if they have a family history of chronic illness or other health concerns.

- Health Insurance: As you approach retirement age, health insurance becomes a bigger concern, especially if you're planning to transition out of employer-sponsored coverage. Consider looking into supplemental health insurance or long-term care options.

- Life Insurance: If your children are financially independent, you may not need as much life insurance. You might want to adjust your policy to reflect any debts or estate planning needs instead.

- Long-Term Care Insurance: At this stage, long-term care insurance becomes a priority. This will cover the cost of nursing home or in-home care should you require assistance in the future.

- Homeowners Insurance: If your children are no longer living at home, you may decide to downsize or move into a new home. Make sure your homeowners insurance covers your new living situation and any changes in property value.

- Health Insurance: At this point, Medicare will likely become your primary health insurance coverage. However, you may still need supplemental insurance supplemental insurance to cover what Medicare doesn’t, such as dental, vision, or prescription drugs.

- Long-Term Care Insurance: If you haven’t already, consider purchasing long-term care insurance, which can help cover the cost of assisted living, nursing homes, or home care if needed as you age.

- Life Insurance: Life insurance can still be useful for estate planning and to leave a financial legacy to your family or charity. If you no longer have dependents, you may opt for a smaller policy or even consider canceling it.

- Homeowners Insurance: Your home may be paid off by now, but homeowners insurance is still important to protect your property and assets. Consider reviewing your coverage as you may no longer need as much coverage for things like personal liability.

- Medicare Advantage or Supplemental Plans: If you qualify for Medicare, you may also want to consider a Medicare Advantage Plan or Medigap policy to ensure you have comprehensive coverage as you age.